July 15, 2026 in

The Family Meeting (Henry series cont.)

When "have we got enough?" becomes "what is it all for?" Brian and Carol came back from three months away looking ten years younger. They...

November 25, 2025

Most people still believe that pensions sit outside their estate when it comes to inheritance tax (IHT). Until recently, they were right. But a quiet policy shift, now legislated to take effect in April 2027, will change the way pension wealth is treated on death. And the implications are significant.

For decades, pensions have been considered a valuable tool not just for retirement income, but for legacy planning. A well-managed pension pot could be passed tax-free to beneficiaries, provided the holder died before age 75. Even after 75, while beneficiaries would pay income tax on withdrawals, the pension itself would remain outside the estate for IHT purposes.

But from April 2027, unused pension funds will be pulled into the taxable estate on death. That means for those who die with unspent pension wealth, HMRC may now take a 40% slice.

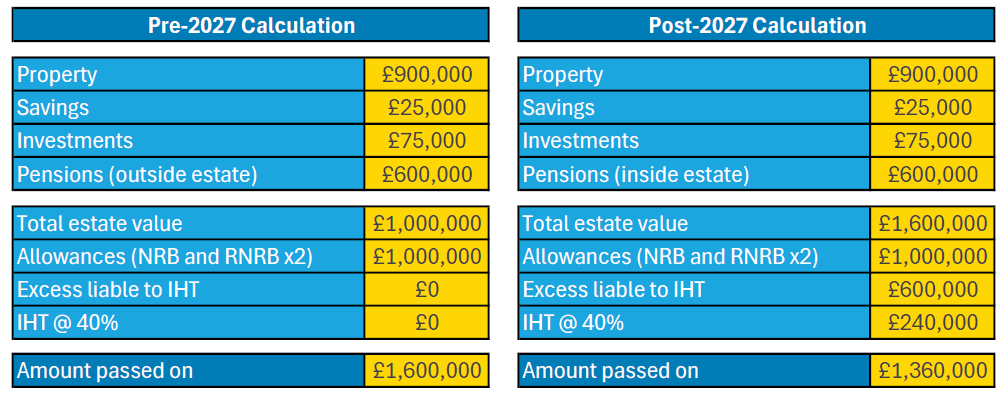

The Numbers: A Simple Example

To highlight the change, we created a simple illustration (see below). The example assumes a married couple with a combined estate of £1.6 million, including a home worth £900,000, savings and investments totalling £100,000, and a remaining pension fund of £600,000. Both full Nil-Rate Bands (NRB) and Residence Nil-Rate Bands (RNRB) are assumed to be available.

Before April 2027: the pension is excluded from the estate. Resulting IHT = £0.

After April 2027: the pension is included in the estate. Resulting IHT = £240,000.

That’s a £240,000 tax increase, solely from a legislative shift.

A Simple Scenario – With Layers

While this illustration is straightforward, it’s just the tip of the iceberg. Estates that exceed £2 million face further complexity: the Residence Nil-Rate Band tapers down by £1 for every £2 above the threshold. That means wealthier families could lose some or all their additional IHT allowance, pushing their liability even higher.

And this doesn’t even account for other traps: lifetime gifts, trusts, and pension withdrawals made late in life can all affect the eventual IHT bill.

Why This Matters Now

This week’s Budget may still throw in surprises. The 2027 legislation could be tweaked, postponed, or even scrapped. But as it stands today, this is a live and pressing risk for families who have worked hard to build long-term wealth.

With frozen thresholds, rising asset values, and stealth changes like this, more people are being pulled into the IHT net – not just the super-wealthy. For couples who believe their pensions are protected, this is a wake-up call.

What You Can Do

The good news? With thoughtful planning, much of this can be managed. Structuring pensions, making timely use of allowances, rebalancing estate assets, and reviewing beneficiary nominations can all help mitigate the impact.

Every situation is different. But what is universal is the need to understand these changes and act early.

Assumptions

Based on a married couple, with both Nil-Rate Band (NRB) and Residence Nil-Rate Band (RNRB) fully available on second death (combined allowance of £1 million). Assumes no gifts or trusts in the preceding 7 years. Pension funds remain exempt from Inheritance Tax (IHT) when passed to a surviving spouse; however, under current legislation, the value is assessable for IHT on second death from April 2027 onwards.

Disclaimer

This illustration is for information purposes only and should not be construed as tax or financial advice. Individual circumstances vary and tax legislation may change. For personalised advice, please speak to a regulated financial planner.

July 15, 2026 in

When "have we got enough?" becomes "what is it all for?" Brian and Carol came back from three months away looking ten years younger. They...

December 5, 2025 in

In the months leading up to the Autumn Budget, thousands of people withdrew funds from their pensions amid speculation that the rules around...

October 7, 2025 in

There’s been a noticeable buzz around pension lump sums (PCLS) in recent months, with more people than ever considering taking tax-free cash...